Securing an SBA loan is often a critical step for entrepreneurs and small business owners who want to grow their businesses. With many SBA-backed loans, a frequent requirement that can catch borrowers off guard is the need for life insurance as collateral.

Whether you’re applying for an SBA 7(a), 504, or have an existing EIDL (Economic Injury Disaster Loan), the lender will likely require a life insurance policy to protect against the unexpected loss of a key person or business owner.

In this guide, we’ll explore what life insurance for SBA loans entails, why it’s necessary, and how to buy the right key man life insurance policy at the right price without delay or headaches.

Why Does An SBA Loan Require Life Insurance?

The U.S. Small Business Administration (SBA) Loan Program is designed to help prospective business owners and existing small businesses secure funds to start a business or expand their operations. The SBA’s role is not to lend money but to guarantee a portion of the loan. The SBA guarantee reduces lender risk. In some cases, they guarantee up to 85% of the total loan amount. The SBA loan guarantee makes it easier for businesses to access capital.

SBA loans are administered by a participating lender, usually a bank or a Certified Development Company (CDC). The lender initiates the loan, and if the SBA agrees to provide guarantees, the lender funds and services the loan.

The SBA offers several types of loans, including the 7(a) Loan Program and the 504 Loan. The 7(a) Loan Program is the most common SBA small-business loan.

In many instances, the SBA requires lenders to obtain life insurance on the borrower as a condition of the loan. The chief reason is the “key man” risk inherent in many small businesses. Most borrowers are smaller companies that rely on one or two “key” people for success. In the event of the death of a key person, the company may not survive, thereby jeopardizing the loan. A key man life insurance policy can guarantee the loan is paid.

The Lender and Development Company Loan Programs Manual, administered by the U.S. Small Business Administration’s Office of Financial Assistance, includes language regarding life insurance requirements. This exhaustive document is an excellent resource for all things concerning SBA Loan Programs.

The latest verbiage for why the SBA requires life insurance can be found in the SOP 50 10 8. Under the SOP 50 10 8 Section B, it states,

- For Standard 7(a), EWCP, CAPLines, International Trade loans and pilot programs (unless specified otherwise in the pilot program guide), 7(a) Lenders may follow their internal policy for similarly-sized non-SBA guaranteed commercial loans, except if the loan is not fully secured, life insurance is required in the amount of the collateral shortfall for the principals of sole proprietorships, single member LLCs, or for businesses otherwise dependent on one owner’s active participation.

- For 7(a) Small Loans, SBA Express and Export Express loans, SBA Lenders may follow their internal written policy for their similarly-sized, non-SBA guaranteed commercial loans.

The following guidance on life insurance applies to all 7(a) and 504 loans:

7(a) Loans

- For Standard 7(a), EWCP, CAPLines, International Trade loans and pilot programs (unless specified otherwise in the pilot program guide), 7(a) Lenders may follow their internal policy for similarly-sized non-SBA guaranteed commercial loans, except if the loan is not fully secured, life insurance is required in the amount of the collateral shortfall for the principals of sole proprietorships, single member LLCs, or for businesses otherwise dependent on one owner’s active participation.

- For 7(a) Small Loans, SBA Express and Export Express loans, SBA Lenders may follow their internal written policy for their similarly-sized, non-SBA guaranteed commercial loans.

504 Loans

CDCs must assess whether the viability of the business is tied to an individual or individuals. Life insurance is required for the principals of sole proprietorships, single member LLCs, or for businesses otherwise dependent on one owner’s active participation when the SBA Loan is not fully collateralized.

- If the CDC determines the principal is uninsurable, the CDC must obtain written documentation from a licensed insurer of the same.

- For each policy required under this Paragraph, CDCs must obtain a collateral assignment identifying the CDC/SBA as assignee that is acknowledged by the Home Office of the Insurer. CDCs must ensure that the Applicant/Borrower pays the premiums on the policy (13 CFR § 120.970(c)).

- CDC may accept the pledge of an existing life insurance policy. Credit life insurance or whole life insurance should not be required.

- When required, the minimum term of life insurance is:

- 10 years for a 10 year debenture.

- 20 years for a 20 or 25 year debenture.

- For the purpose of life insurance calculation, the loan is considered fully collateralized when the value of the discounted collateral is equal to or greater than the net debenture amount. When the loan is not fully collateralized, the amount of life insurance required is equal to the difference between the net debenture amount and the value of the discounted collateral.

- For life insurance only, the calculation of discounted collateral is as follows:

- Improved real estate at 85% of fair market value determined in accordance with the appraisal requirements in Section C, Ch. 1, Para. E.2.b., Appraisals.

- New machinery and equipment (excluding furniture and fixtures) at 75% of price minus any prior liens.

- Used or existing machinery and equipment (excluding furniture and fixtures) at a maximum of 50% of Net Book Value or 80% with an Orderly Liquidation Appraisal minus any prior liens.

Sample Rates on Life Insurance to Cover an SBA Loan

All rates in the table below are guaranteed for 10 years and include policy options requiring an insurance exam, as well as those that do not. All life insurance rates quoted are based on annual payments (other payment modes available) and assume the top non-tobacco health class for both male and female. Rates are from A+ Rated insurance providers and are subject to change.

10 Year Term Life Insurance to Cover an SBA Loan

| Ages | $250,000 | $500,000.00 | ||||||

|---|---|---|---|---|---|---|---|---|

| Exam | No Exam | Exam | No Exam | |||||

| M | F | M | F | M | F | M | F | |

| 30 | $107 | $100 | $154 | $119 | $155 | $140 | $210 | $150 |

| 40 | $127 | $125 | $187 | $161 | $195 | $185 | $273 | $203 |

| 50 | $275 | $223 | $312 | $263 | $485 | $395 | $525 | $438 |

| 60 | $663 | $490 | $785 | $564 | $1,225 | $870 | $1,463 | $956 |

| 65 | $1,105 | $768 | N/A | N/A | $2,110 | $1,400 | N/A | N/A |

Within the term life insurance category, there are several policy types.

- Decreasing Term Life Insurance: Decreasing term usually has a fixed cost with a declining insurance amount over time. These policies were used years ago to protect mortgages. They were really inexpensive, and the amount of insurance decreased over time as you paid down your outstanding mortgage. It would seem that a decreasing term life policy would be ideal for covering an SBA loan. However, today you can buy a level term policy with a fixed rate and a fixed benefit for less than it would cost to buy a decreasing term plan.

- Annual Renewable Term Life Insurance (ART): Annual renewable term policies provide a fixed amount of insurance with a rate that increases every year. These plans are generally really cheap for the first 2-3 years. However, they are not cost-effective in the long term. If your loan term is very short, you may consider an ART policy, but if the loan payoff is longer than 3 years, a level term plan will be more cost-effective.

- Level Term Life Insurance: Level term offers a fixed rate for insurance for a fixed number of years and is guaranteed not to change during the level term period.

- No-Exam Term Life Insurance: No-exam level term is exactly what it sounds like: level term life insurance that does not require a medical exam. These policies are a first option if you need coverage fast. They are always slightly more expensive, but in some cases, timeliness is the most critical factor. No one wants to wait 3-4 weeks for a life insurance policy to be approved when the bank is ready to close on their loan. With no-exam term life, you can usually lock in coverage quickly, allowing you to close on the loan faster. In some cases, you can be approved for coverage in as few as 2-3 days

With that said, level term insurance plans are the most popular choice for satisfying SBA loan insurance requirements for several reasons:

- They are the least expensive policy option for loans with durations longer than 3-4 years.

- They are perfect for tailoring a policy to match the loan’s exact maturity. For example, if you have a 10-year note, you can buy a 10-year term policy to essentially lock in your cost and guarantee your insurance amount for the life of the loan. There are even plan options that can “dial-in” the level term period to the exact term of the note. For example, if your note is 18 years, there is an 18-year level term option.

- You can drop the policy at any time without penalty. If you pay off your loan faster than expected, you can cancel the policy simply by discontinuing premium payments.

Other life insurance policies, such as whole life, universal life, index universal life, or variable universal life, can also be used to secure an SBA Loan. However, buying one of these policies solely to meet a lender’s requirement is not advisable.

Whole life insurance or universal life is protection designed for situations where coverage is needed for life, or where cash accumulation is a primary goal.

Like term insurance, permanent insurance comes in many variations. These policies have many attractive features and benefits, including cash value potential and lifetime guaranteed insurance for the key person.

Permanent life insurance would be an attractive solution only for more mature companies with significant cash flow. Companies in this position normally have assets and other collateral that can be used to guarantee any SBA loan.

In these instances, life insurance would not normally be required by the lender or the SBA. Therefore, permanent insurance is rarely purchased to satisfy the collateral requirement for an SBA loan.

How Long Does it Take to Get a Life Policy in Place?

The truth is, it depends. Numerous factors can shorten or lengthen the time it takes to get a policy approved.

The timeline will largely depend on your health and medical history. It can take anywhere from 48 hours to four weeks. Wherever you fall in that range, don’t worry. We have multiple avenues you can take and platforms you can use to compare quotes and find the right policy.

No matter your situation, we can guide you down the path to find the right policy at the best possible price.

Check out our key man insurance underwriting guide to see how your situation measures up against most insurance companies. If you work with an agent who isn’t knowledgeable about your specific health issue, then you are wasting your time and money – especially when it comes to securing an SBA loan. More often than not, the sole remaining item necessary to close on an SBA loan is proof of coverage.

We have worked with virtually every medical condition (including heart disease, diabetes, sleep apnea, and cancer), and have been very successful at helping people who have been declined in the past and struggled to find the best life insurance for an SBA loan.

If you cannot qualify for traditional life insurance, there is another option called “Failure to Survive.”

How Collateral Assignments are Used to Meet SBA Loan Life Insurance Requirements

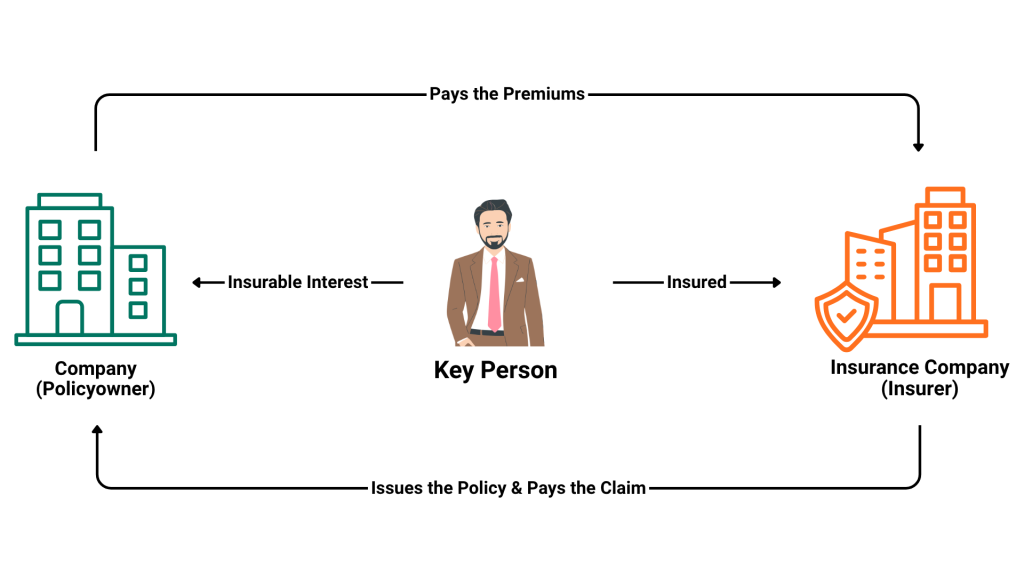

The whole purpose of securing a key man life insurance policy is to satisfy the SBA loan insurance requirements. When naming the beneficiary, it is important that you set up the policy to meet the lender’s conditions.

How Keyman Insurance Works

The structure of a key person insurance policy is straightforward. The business purchases and pays the premiums for a life or disability insurance policy on the key employee’s life. In return, the life insurance company promises to pay a benefit to the business if the covered employee dies or becomes disabled.

As with all key man life insurance, if the business is making the loan, the proper thing to do is to name your business, not the lender, as the primary policy beneficiary. Under this scenario, the company will:

- Own the policy

- Pay the premiums

- Receive the proceeds

Any variation from this method is NOT recommended.

How Collateral Assignments Work

Take the above scenario and add one more element to it:

The company will:

- Own the policy

- Pay the premiums

- Receive the proceeds

- AFTER the Assignee (Lender) receives the outstanding loan balance.

A collateral assignment is a legally binding document familiar to every bank and lending institution. In fact, both lenders and life insurance companies have their own variations of collateral assignments.

A collateral assignment places the lender or bank in a primary lien position for any death benefit payout of policy proceeds. Once the key man life policy is effective, both the lender (bank) and the policy owner (the business) sign a collateral assignment.

The business that owns the policy is commonly referred to as the “assignor,” and the bank is referred to as the “assignee.”

The agreement is then sent to the insurance company to be recorded as binding in the official policy file. Copies of the recorded assignment are then sent to the lender or “assignee” as proof that they have the first rights to the policy proceeds in an amount equal to the loan balance in the event of the key person’s death.

At the death of the key person, the bank receives only the loan payoff balance, and the remainder of the death benefit is payable to the primary beneficiary, the company.

Let’s go through a quick example:

ABC Company, owned by John Smith, has taken out a $1,000,000 loan from DEF Bank, which was guaranteed by the SBA. As part of the deal, ABC purchased a key man life insurance policy for $1,000,000 on the life of John Smith, with ABC as the primary beneficiary.

Prior to the closing of the loan, a collateral assignment was signed by John Smith, the assignor, and DEF Bank, the assignee, and made effective by the insurance company.

Six years later, the loan balance was $675,500.00 when John Smith suddenly passed away. Upon the payment of proceeds, the insurance company notices that a collateral assignment is in effect, naming DEF as the assignee.

DEF is notified by the insurance company and submits proof of the outstanding loan balance. A check is then made payable to DEF Bank for $675,500, which satisfies the outstanding loan balance.

The remaining $324,500 is payable to ABC Company.

The main advantage of a collateral assignment is that the lender (DEF) receives only the proceeds equal to the outstanding loan balance.

If the DEF had been made the primary beneficiary, at John Smith’s death, they would have received a check for $1,000,000. This would obviously be a problem for ABC Company.

Under no circumstances is it ever advisable to name a lender the beneficiary of a key man life insurance policy.

Once the loan is paid off, the bank will release any collateral assignment. A simple form needs to be signed and submitted to the insurance company for the assignment to be released.

Many years ago, our office helped a general contractor from Hawaii secure key person insurance. The contractor was a very successful builder, but relied on “investors” and “private lenders” to finance large projects and developments. He had ongoing agreements with these creditors as each job was completed, he rolled the financing into a new, larger project. As such, the lenders required him to maintain $3,000,000 in key person insurance and mandated that they be the policy beneficiary.

The creditors sought protection in case of the contractor’s unexpected death during the project. We strongly cautioned the contractor NOT to name the lender the beneficiary of the policy and, alternatively, recommended a collateral assignment. Even after we explained the downside to naming the lender as a beneficiary, the contractor was ok with that structure.

Turn the page ten years, and the policy was still active. We received a call from a relative of the Hawaiian contractor inquiring about the insurance policy and notifying us of the death of the contractor. Unfortunately, we confirmed that there was a $3,000,000 policy, but the primary beneficiary was the lender and not the contractor’s business or family. The family was only a 10% beneficiary.

The ultimate irony was that at the time of his passing, the contractor was retired and owed nothing to the lender. If the contractor had named his company or family the beneficiary, and executed a collateral assignment naming the lender the assignee. The business or family would have received $3,000,000 tax free. This was a very costly mistake that you want to avoid.

Do’s and Don’ts when Buying Life Insurance for SBA Loans

First, let’s discuss what NOT to do so you can avoid the common pitfalls of improperly set-up policies.

DON’T Wait Until The Last Minute. If you do not give yourself enough time to apply for the key man life insurance, you may be forced to go the no-exam route, which may not make sense otherwise. As mentioned, doing an exam nearly always saves you money. Also, if you start early, you can be prepared for the unexpected. For example, you may need to transition from one company to another to get the best rate. By starting early, you give yourself the time and flexibility to go to “Plan B.”

DON’T Withhold Important Medical and Health Information: This point cannot be overstated. If you are not upfront about your health details, you will waste time and overpay!

DON’T Let Your Policy Lapse: Once the key man policy is in effect, pay your premiums when due. In the unfortunate event your policy lapses, the lender may default the loan or you may have to go back through the underwriting process, which may prove costly.

Now, here are some things you can do in order to get the best life insurance for an SBA loan at a faster approval with lower rates.

DO Consider the Exam Route: As noted, the exam option will always result in the lowest rates. Unless you are extremely healthy, under the age of 60, need $500,000 or less in life insurance, and don’t mind paying more, undergo the exam when applying for life insurance for an SBA loan.

DO Use a Broker to Assist You: That’s right, only by working with an independent agent, who represents many insurance companies, will you give yourself the best chance of getting the right insurance policy at the best possible price.

DO Use a Collateral Assignment: Never name the lender as a beneficiary on any key man life insurance policy. Collateral assignments are easy to implement and will protect both you and the lender. And, they are readily accepted by lenders to satisfy the existing collateral requirements for all SBA loans.

Common Questions About SBA Life Insurance Requirements

How long does it take to get a key man life insurance policy?

That depends upon your age, health, and your choice of insurance company. The biggest factor is health. If you are young and healthy and fall under the guidelines for a no-exam policy, you may get approved for coverage within 2-3 days. However, this is not the norm.

If you are in good health and are willing to complete an insurance exam (which we recommend in most cases), you can be approved in as little as 2 weeks. This assumes that your medical reports are not ordered from your physician(s). The normal processing time for people without significant health histories who do an insurance exam is 3-4 weeks.

If you have a history of medical conditions, all insurance companies will require medical reports from your attending physicians. This is a routine requirement and can extend the underwriting time to 4-6 weeks. The key to shortening this window is how quickly your doctors will respond to the request for your records – or alternatively, access the records yourself.

How much does a key man insurance policy cost?

Ultimately, the cost of any key man life insurance policy is determined by three things: age, health, and the amount and duration of the insurance policy. We have provided sample rates in this article. You can also get an instant key man life insurance quote here.

Which life insurance companies are best?

We represent over 80 insurance companies. The reality is that there are only about 30-35 life insurance companies that are ultimately competitive. The key is to match your health circumstances with the company that will look at you most favorably in underwriting. As mentioned previously, working with a broker who has the underwriting expertise is going to guarantee that you choose the right company!

What if I am uninsurable?

Although rare, there are situations where life insurance is just not an option due to health conditions. In these cases, the SBA/Lender Guidelines are as follows:

If the lender determines the principal is uninsurable, the lender must obtain written documentation from a licensed insurer of the same.

In most cases, after attempting to get a life insurance policy and being “denied” due to a medical condition, the lender will accept written proof from a licensed insurance company that claims you are uninsurable. At this point, it will be up to the lender’s discretion how the loan is handled.

Can I cancel the key man insurance policy?

Yes, life insurance policies are “unilateral contracts”, which means the policy can be canceled at any time, without penalty, by simply stopping premium payments. If you pay off your loan early, you can cancel the key man life policy at any time.

Looking to Secure a Life Insurance Policy for Your SBA Loan? Here Are Your Next Steps

As you can see, the literature, requirements, and options around securing life insurance for an SBA loan are extensive.

If we could boil this article down to the essentials, this is what we recommend doing:

Research

While the process may seem daunting, we recommend breaking down your search for a life insurance policy into the following steps:

- Identify What the Lender Requires. The bank will tell you exactly what they need to satisfy their requirements. These are your marching orders.

- Shop Around. This is more than just going to a website and getting rates. What you get in a quick quote is unlikely to be what you’re offered in the end. There are many factors to consider, and an experienced agent will make sure that no stone is left unturned.

- Talk to a Pro. Thoroughly review your situation and listen carefully. Tell them about your medical history and any other important information that may impact your rates, such as scuba diving, tobacco use, moving violations, etc.

- Discuss Your Options. Ask questions about the insurance company’s financial strength link to FRG?. Are there any features or benefits that make one policy better than another? While price is the number one concern, there may be policies priced the same that offer equally priced policies, with one company offering significantly better features.

Apply

Once you have found a policy that is right for you, review and complete your application, sign it, and submit it to the agent for processing to the insurance company. If you are doing an exam, remember to fast prior to your appointment. For more on this, read our guide and checklist for an insurance exam.

Get approved

After a few weeks, your policy is approved. Hopefully, your exam results are good, and you are approved at the rate applied for. At this point, all that is required is a premium payment and a few signatures to make the policy effective.

While you will likely effect a collateral assignment with the lender, you will be expected to record the agreement using the insurance company’s own proprietary form as well.

That’s it! You have satisfied the collateral requirements to finalize your SBA loan. Now all you need to do is execute your plan to realize your vision!

Contact us right away to get started.